- New Money

- Posts

- Overwhelmed

Overwhelmed

A beginner shortcut to finally know what to invest in

Angelo Castillo

April 07, 2026

Happy Tuesday,

Angelo here! Welcome to New Money, where we go over weekly tips to help you build your wealth, one dollar at a time.

Today’s edition:

The beginner’s investing shortcut

ETFs vs index funds made simple

Rising costs, tech risks, and more…

Read time: 2 min 30 seconds

🍎Wealth Tip of the Week

When I first opened my brokerage account, I did what every confused beginner does.

I Googled "how to start investing" and hit a wall.

Not a complexity wall. An options wall.

There was an S&P 500 index fund. Right next to it, an S&P 500 ETF. Same company. Same 500 companies inside. Nearly identical fees.

A 2024 Janus Henderson report found that nearly half of Americans are not investing at all and most of them say the reason is confusion, not a lack of cash.

I spent too long researching which ones were "better" instead of just investing. Meanwhile, the market kept moving without me.

When everything looks almost identical, your brain treats the decision like it matters more than it does.

That time was not wasted though. I came out the other side actually understanding them.

Let me lay out the key differences, what actually matters, and which one makes the most sense for you so you can move forward knowing exactly what you’re investing in.

1. The Four Ways to Invest

I remember thinking: “Okay… but what am I actually supposed to choose?”

Because suddenly, you’re hearing all these terms:

Individual stocks

ETFs

Index funds

Mutual funds

And it feels like picking the wrong one could mess everything up when you’re starting. So let’s get into them.

Individual Stocks. This is where most people naturally go first.

You pick one company like Apple, Tesla, Nvidia and hope it grows. If it does, you win big. If it doesn’t, you feel it immediately.

It sounds like the fastest way to make money. But in reality, you’re taking on more risk than you realize especially if you don’t fully understand the business.

And when things go wrong, it’s much harder to stay calm. So you sell too early and lose confidence. It is the highest-risk starting point with the steepest learning curve.

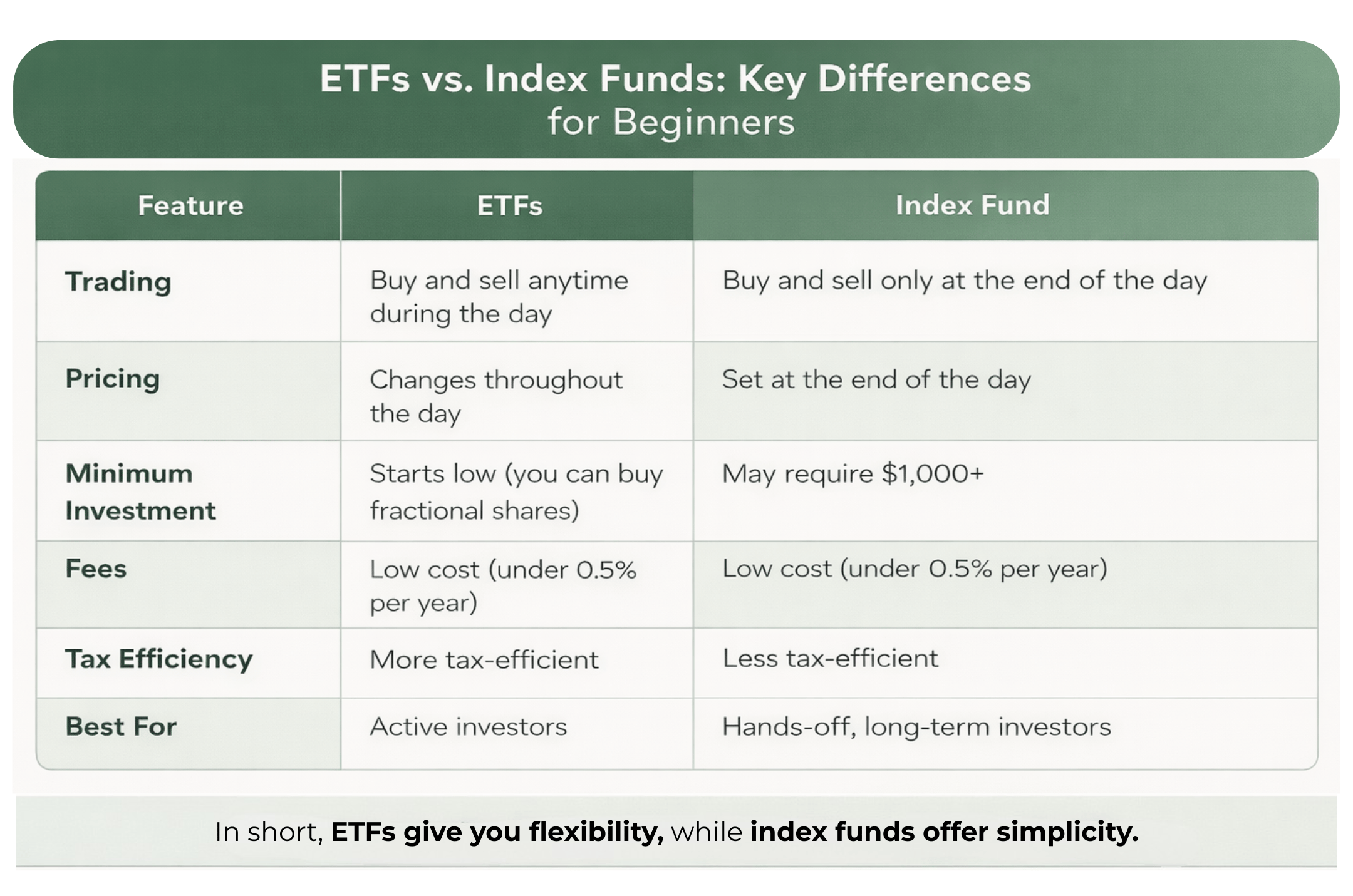

ETFs (Exchange-Traded Funds). This is where things started to make more sense for me. Instead of picking one company, you invest in many at once.

Think of it like this: Instead of trying to guess the winner, you stop trying to beat the market and start owning it.. You can buy and sell ETFs anytime during the day, just like a stock.

They’re flexible, low-cost, and easy to understand once you see the bigger picture.

Index Funds. Index funds do the exact same thing as ETFs. It’s the same idea, the same companies, and the same goal. The only real difference is how you buy them.

You can only invest once per day, which actually makes it more hands-off. It limits second-guessing and keeps you consistent.

Mutual Funds. This is what a lot of people get pushed into early on. Someone manages it for you, picks the investments, and tries to beat the market.

But here’s the part most people don’t hear: they usually come with higher fees and most of them don’t outperform simple index funds over time.

S&P Dow Jones SPIVA Report - SPIVA

In fact, according to the S&P Dow Jones SPIVA report, around 70–80% fail to beat the market in many years.

So you end up paying more… for similar or worse results.

2. What Works When Starting Out

If you’re just starting, here’s the truth:

You don’t need to pick the perfect investment.

You need to pick something that:

Keeps your risk low

Keeps things simple

Helps you stay consistent

That’s why the best place to start is with: 👉 ETFs or index funds

Instead of trying to guess which company will win, you invest in all of them.

It’s less stressful and more consistent. You’re not trying to be right once.

You’re setting yourself up to be right over time.

3. Index Funds vs ETFs

Now you’re choosing between index funds and ETFs. And honestly, it’s much simpler than it sounds.

ETFs are generally more tax-efficient. They’re designed in a way that avoids triggering taxes as often.

Index funds can sometimes create small taxable events in the background.

In retirement accounts, this doesn’t matter much

In regular accounts, ETFs can save you money over time

Let’s say you invest $10,000 for 20 years at around 7% per year:

ETF (0.05% fee) → about $1,000 in fees

Index fund (0.15% fee) → about $3,000 in fees

It looks like a tiny difference.

But over time, those small percentages quietly add up.

If you want a deeper but still beginner-friendly breakdown of ETFs, I recommend watching 👉this video. It’ll give you a clearer picture of how ETFs actually work and what to watch out for before you start.

4. Your 2026 Starting Plan

Here’s how to start:

Step 1: Open a brokerage account.

Choose a platform like Webull, Fidelity, Vanguard, or Schwab.

They’re all beginner-friendly and reliable.

It takes about 10 minutes to set up.

Step 2: Pick your base investment

Start with something simple that tracks the S&P 500.

You can choose:

An ETF (more flexible)

Or an index fund (more automated)

Both give you instant diversification across hundreds of companies.

Step 3: Keep your fees low

Look for an expense ratio below 0.10%.

It sounds small, but over time, fees quietly eat into your returns.

Step 4: Automate it

Set up a recurring investment even just $25 or $50 a month.

This removes overthinking and builds consistency.

Step 5: Stay in the game

Don’t check it every day. Don’t try to time the market.

Just keep investing and let compounding do its job.

The market doesn’t care how much you start with.

It cares how long you stay in.

One honest note: you can use both. Use index funds for automatic monthly investing, and ETFs for specific sectors like tech or global markets.

That works well once you’re more comfortable.

But for now, don’t overcomplicate it.

Pick one. Start. Stay consistent.

Are you still overthinking… or are you finally going to start? Hit reply

I read every response :)

Where are you right now in your financial journey? |

💬Quote of the Week

It is a universal principle that you get more of what you think about, talk about, and feel strongly about.

📉 Market Recap

Check out some of the biggest stories shaking up money, markets, and momentum this week.

👉Trump escalates threats as Iran tensions rise

Trump warned of major attacks on Iran’s infrastructure if no deal is reached, while both sides continue sending mixed signals and launching strikes.

Wallet impact: Ongoing conflict keeps oil markets unstable, expect potential spikes in gas prices and rising costs across everyday goods.

👉Meta and Google found liable in social media addiction case

A jury ruled that Meta and Google must pay $6M, saying their platforms contributed to user addiction among younger users. More lawsuits could follow.

Wallet impact: If more lawsuits happen, big tech companies may face higher costs, which can reduce profits and put pressure on their stock prices over time.

👉USPS plans 8% delivery surcharge as fuel costs rise

USPS plans to add an 8% delivery fee to cover rising fuel costs, which could increase shipping prices if approved.

Wallet impact: PShipping will get more expensive. If you buy or sell online, expect higher delivery costs and possibly higher prices on products to cover those fees.

👉OpenAI raises $120B as AI demand explodes

OpenAI is raising $10B, pushing its total funding past $120B as AI demand surges and IPO plans build.

Wallet impact: AI is becoming a major investment trend, creating new income opportunities but also accelerating changes across industries.

As of 04/06/2026

I want your honest take! Are you enjoying the market recap? |

👀 In Case You Missed It

By 24, I made $529,640.83 across 10 different income streams and in this video, I’m breaking down exactly what they are and how they work.

🌱3 more ways I can help build your wealth

Budget Template + Net Worth Tracker: Most budgeting apps either baby you or confuse you. This template does neither. It gives you clarity in under 10 seconds a day. I use it to track spending, savings, and net worth in one place.

My Youtube Channel: If you prefer learning visually, I walk through real-life examples, portfolio breakdowns, and beginner-friendly concepts step by step so they actually make sense.

Quick Survey (Help Me Help You): The more I understand you, the better I can guide you. It only takes 2 minutes to fill this out so I can help you create structure and build wealth with confidence.

See y’all next week 🫡

Angelo Castillo

How did you like today's newsletter? |

Disclaimer: The content of this newsletter is for informational purposes only and should not be construed as investment, legal, or tax advice. The views and opinions expressed herein are solely those of the author and do not necessarily reflect the views of any business, employer, or other entity. Investing involves risks, including the potential loss of principal. Past performance does not guarantee future results. Readers are advised to conduct their own research and consult with qualified professionals before making any investment, legal, or financial decisions. The information provided is believed to be accurate but cannot be guaranteed. The author and publisher disclaim any liability for actions taken based on the content of this newsletter. This newsletter is not an offer to buy or sell any security. By subscribing or continuing to read this newsletter, you acknowledge and accept these terms and conditions.

Some of the links are my affiliate links. If you click on these links and sign up/purchase something, I may earn a small commission at no additional cost to you. This helps support me and allows me to continue creating content for you. I only promote products and services I genuinely believe in. Thank you for your support!